CHAPTER 50:01 – CUSTOMS AND EXCISE DUTY*: SUBSIDIARY LEGISLATION

INDEX TO SUBSIDIARY LEGISLATION

Customs and Excise Duty Regulations

* Customs and Excise Duty Act repealed by the Excise Duty Act 34 of 2018.

CUSTOMS AND EXCISE DUTY REGULATIONS

(section 130)

(28th March, 1974)

ARRANGEMENT OF REGULATIONS

REGULATION

PART I

Preliminary

1. Citation

2. Interpretation

PART II

Administration, General Duties and Powers of Director and Officers, and

Application of Act

3. Officers to perform temporary and additional duties

4. Officers required to undertake extra attendance

5. Production of authority by officer

PART III

Importation, Exportation and Transit of Goods

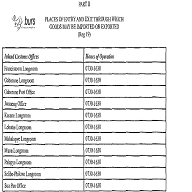

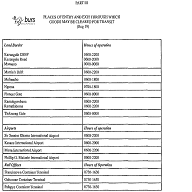

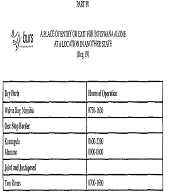

6. Appointment of places of entry, authorised roads and routes, etc.

7. Landing of aircraft at places not appointed for that purpose

8. Report of arrival or departure of aircraft

9. Boarding and searching of aircraft

10. Aircraft stores

11. Landing of goods from aircraft: deposit of goods in transit shed

12. Delivery of goods from airports and railway goods depots

13. Exportation of goods

14. Importation or exportation of goods from and to African territories

15. Persons and their baggage entering or leaving the common customs area

16. Rent to be paid on goods in a State warehouse

17. Removal of goods in bond

PART IV

Customs and Excise Warehouse: Storage and Manufacture of Goods in

Customs and Excise Warehouses

18. Approval of customs and excise warehouses

19. Storage of goods in customs and excise warehouses

20. Transfer of ownership of dutiable goods in warehouse

21. Manufacture of goods in customs and excise warehouses

22. Clearance and removal of goods from customs and excise warehouses and payment of duty

23. Clearance and removal of goods from customs and excise warehouses for home consumption

24. Clearance and removal of goods from customs and excise warehouses for export (including supply as stores to foreign-going aircraft)

25. Clearance of goods from customs and excise warehouses for removal in bond

26. Ascertaining the strength and quantity of spirits for duty purposes

27. Control of the use of spirits for certain purposes

28. Requirements in respect of stills

29. Spirits manufactured by agricultural distillers

30. Manufacture of spirits in customs and excise manufacturing warehouses

31. Manufacture of spirituous beverages in any customs and excise storage warehouse and clearance of such beverages

32. Manufacture of wine

33. Manufacture of beer

34. Manufacture of vinegar substitutes, etc.

35. Manufacture of tobacco

36. Manufacture of mineral oils

37. Manufacture of motor vehicles

38. Manufacture of sales duty goods

PART V

Clearance and Origin of Goods: Liability for and Payment of Duties

39. Entry of goods and time of entry

40. Requirements regarding invoices

41. Origin of goods

42. Importation of cigarettes

PART VI

Anti-Dumping Duties

43. Onus of proof

44. Currency conversion

PART VII

Application of Agreements with other African Territories

45. General

46. Transfer of goods between the partner states

PART VIII

Amendment of Duties

47. Amendment of duties

PART IX

Licensing

48. Issue and renewal of licences

49. Licensing of special customs and excise warehouses

50. Allocation of numbers to customs and excise warehouses

51. Issuing and renewal of licences to agricultural distillers

52. Special provisions regarding stills and still makers

PART X

Value

53. Foreign currency

54. Exemptions

55. Related persons

56. Valuation code on bill of entry

57. Valuation methods

58. Furnishing of information

59. Valuation determination

60. Method of determining value

61. Additions to price

PART XI

Rebates, Refunds and Drawbacks of Duty

62. General provisions

63. Registered premises

64. Rebate stores

65. Security

66. Liability for duty

67. Transfer of goods

68. Stock records and working cards

69. General refunds in respect of imported, excisable or sales duty goods

PART XII

Penal Provisions

70. Penal provisions

PART XIII

General

71. Removal of excisable goods within the common customs area

72. Examination of goods

73. Wreck

74. Goods unshipped or landed from wrecked or distressed aircraft

75. Days and hours of general attendance

76. Charges for extra and special attendance

77. Business in customs houses

78. Surety bonds

79. Agents and carriers subject to section 111 of the Act

80. Business records to be kept

81. Import and export list

82. Certificates for imported motor vehicles

First Schedule – Requirements regarding Invoices

Second Schedule – Index of Forms

Third Schedule – Industrial Rebates of Fiscal and Customs Duties

Fourth Schedule – General Rebates of Fiscal and Customs Duties

Fifth Schedule – Specific Drawbacks and Refunds of Fiscal and Customs Duties

Sixth Schedule – Specific Rebates and Refunds of Excise Duties

Seventh Schedule – Rebates and Refunds of Sales Duty

Eighth Schedule – Appointment of Places of Entry, Authorised Roads and Routes, etc.

S.I. 36, 1974,

S.I. 82, 1975,

S.I. 108, 1976,

S.I. 28, 1977,

S.I. 79, 1978,

S.I. 152, 1978,

S.I. 93, 1980,

S.I. 34, 1982,

S.I. 140, 1983,

S.I. 167, 1983,

S.I. 18, 1986,

S.I. 20, 1986,

S.I. 61, 1986,

S.I. 97, 1986,

S.I. 132, 1987,

S.I. 26, 1988,

S.I. 92, 1988,

S.I. 83, 1990,

S.I. 79, 1991,

S.I. 118, 1991,

S.I. 131, 1991,

S.I. 57, 1992,

S.I. 29, 1993,

S.I. 45, 1993,

S.I. 22, 1994,

S.I. 68, 1994,

S.I. 121, 1994,

S.I. 124, 1994,

S.I. 56, 1996,

S.I. 79, 1996,

S.I. 34, 1997,

S.I. 6, 1998,

S.I. 42, 1998,

S.I. 43, 1998,

S.I. 76, 2000,

S.I. 37, 2001,

S.I. 8, 2002,

S.I. 30, 2002,

S.I. 47, 2002,

S.I. 38, 2003,

S.I. 61, 2003,

S.I. 127, 2004,

S.I. 88, 2005,

S.I. 49, 2006,

S.I. 84, 2007,

S.I. 58, 2010,

S.I. 62, 2010,

S.I. 64, 2010,

S.I. 27, 2012,

S.I. 147, 2020,

S.I. 9, 2024.

PART I

Preliminary (regs 1-2)

These Regulations may be cited as the Customs and Excise Duty Regulations.

In these Regulations, unless the context otherwise requires—

“examination” includes the use of X-ray scanner;

“foreign-going” means departing from any place within the common customs area to any place outside the common customs area;

“proper officer” means any officer whose right or duty it is to require the performance of or to perform the act referred to.

PART II

Administration, General Duties and Powers of Director and Officers,

and Application of Act (regs 3-5)

3. Officers to perform temporary and additional duties

(1) Any officer may at any time be called upon to perform temporarily duties other than those ordinarily appertaining to his class or grade.

(2) Officers may be called upon at any time to perform, in addition to their normal duties, such clerical work as the Director may decide.

4. Officers required to undertake extra attendance

No officer shall have the right to refuse to undertake extra attendance but the Director may exempt an officer from such attendance in general or in any particular case.

5. Production of authority by officer

Any officer whose normal duty it is to conduct inspection under the Act shall, on arrival at the premises of any importer, manufacturer or any other person on routine inspection duties, declare his official capacity and purpose and produce the authority issued to him by the Director to conduct such inspection, but the provisions of this regulation shall not apply in circumstances which the Director considers exceptional.

PART III

Importation, Exportation and Transit of Goods (regs 6-17)

6. Appointment of places of entry, authorised roads and routes, etc.

(1) The places, roads, routes, sheds, entrances and exits appointed or prescribed under section 7 of the Act and their use or employment for the purposes for which they have been so appointed or prescribed shall be subject to the conditions stated in the Eighth Schedule hereto.

(2) No person shall enter any place appointed under section 7 of the Act, except the persons required by the department to enter it, the proper officers and such other persons as the Director may permit to enter such place.

7. Landing of aircraft at places not appointed for that purpose

(1) The pilot of any aircraft arriving in Botswana from a place outside the common customs area who is forced by stress of weather, accident or other circumstances beyond his control to land at a place in Botswana not appointed as a customs and excise airport (whether or not such aircraft has already called at any place in Botswana), shall forthwith report the arrival of his aircraft in terms of section 8 of the Act and the circumstances of such arrival to the proper officer at that place.

(2) If no customs and excise officer is stationed at the place mentioned in subregulation (1) such pilot shall forthwith report the circumstances of his arrival to the magistrate or a member of the Botswana Police Force at or nearest to that place and such pilot shall also as early as possible make a report in terms of section 8 of the Act to the proper officer at the place at which such aircraft was next due to land or to the proper officer nearest to the place where he has landed.

(3) Such pilot shall forthwith take steps to prevent the landing, loss, damage, removal or pilferage of any cargo or other goods on such aircraft or, if any cargo or other goods are landed from such aircraft when in distress, to prevent the loss, damage, removal or pilferage of any cargo or other goods so landed.

(4) He shall also report available particulars of all cargo or other goods landed from such aircraft to the proper officer, magistrate or a member of the Botswana Police Force.

(5) The pilot of such aircraft shall also prevent the passengers and crew of such aircraft from leaving the immediate vicinity thereof unless the permission of the proper officer, magistrate or a member of the Botswana Police Force has been obtained or the circumstances demand otherwise.

(6) Any magistrate or a member of the Botswana Police Force to whom a report is made by a pilot of such aircraft shall report the circumstances to the nearest proper officer by the most expeditious means available and shall render all possible assistance to such pilot to comply with the requirements of subregulations (3), (4), and (5).

8. Report of arrival or departure of aircraft

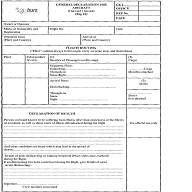

(1) The report referred to in section 8(1)(a) of the Act shall state the information required in the form CE.2 specified in these Regulations.

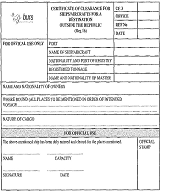

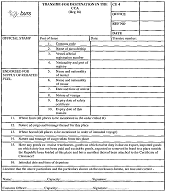

(2) The pilot of any foreign-going aircraft shall, before its departure from any place in Botswana, deliver to the proper officer one general declaration in the form CE.2 in respect of all destinations together and a separate transire in the form CE.4 (Transire-For a Destination in the Common Customs Area) in respect of each such destination.

(3) A manifest, in the form CE.3, of all goods shipped as stores ex customs and excise warehouse and of all excisable and sales duty goods shipped as stores on such foreign-going aircraft (or alternatively copies of all bills of entry for shipment of such goods), shall be sealed by the proper officer to such general declaration.

(4) A manifest, in the form CE.3, of all goods ex customs and excise warehouse or goods on which a drawback of customs or excise duty is due on export or imported goods on which duty has not been paid or excisable or sales duty goods, exported or removed in bond on such foreign-going aircraft to a place outside the common customs area (or alternatively copies of all bills of entry for shipment of such goods), shall be sealed to such general declaration.

(5) A copy of the report outwards in the form CE.2 incorporating copies of the manifests of all goods shipped at that place on such foreign-going aircraft for a destination outside the common customs area (including again the goods mentioned in subregulation (4), shall be sealed to such general declaration.

(6) The pilot of such foreign-going aircraft shall submit, at the time of reporting inwards of such aircraft, to the proper officer at every place in the common customs area at which such aircraft calls, the general declaration issued to him at every place in the common customs area at which such aircraft has previously called and such declaration may be retained by the proper officer until the time of departure of such aircraft.

(7) To the transire submitted in terms of section 8(6) of the Act by the pilot of a foreign-going aircraft in respect of each place in the common customs area at which it is due to call the proper officer shall seal a manifest, in a form approved by the Director, of goods removed in bond or, alternatively, copies of all bills of entry for the removal of goods in bond to that place (or if no goods for removal in bond have been shipped for that place, the relative transire must bear a statement to that effect) and such transire shall contain a statement whether or not goods of the nature referred to in subregulation (3) or (4) have been shipped at any place in the common customs area.

(8) Such transire shall also contain a manifest of goods carried coastwise and shall be handed to the proper officer at the time of reporting inwards of such aircraft at the place of destination and shall be retained by the proper officer at that place.

(9) The proper officer may refuse clearance for the departure of any aircraft from any place unless evidence to his satisfaction has been produced that the pilot of such aircraft has complied with the provisions of all laws of Botswana and the customs laws of the common customs area with which it was his duty to comply.

(10) The pilot of any aircraft arriving at or departing from any place in Botswana shall submit to the proper officer the number of copies of such documents as are referred to in subregulations (1) to (9) as the proper officer requires.

9. Boarding and searching of aircraft

(1) All sealable goods which have not been declared by the pilot or any member of the crew of an aircraft at any place in Botswana under section 9 of the Act and any other goods (not being the personal baggage or possessions of the pilot, crew or passengers) which the pilot is unable to prove to the satisfaction of the proper officer to be manifested for discharge at any other place shall be treated as illicit goods and shall be liable to forfeiture.

(2) The proper officer may prohibit any person who has no official business on such aircraft from boarding the aircraft until such formalities on arrival of the aircraft relating to customs and excise requirements as he may decide have been completed.

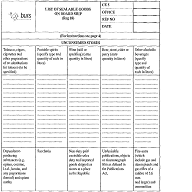

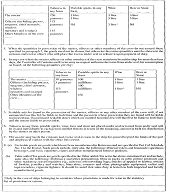

(1) The declaration required under section 9 of the Act shall be made in the form CE.5 and shall be handed to the proper officer on demand immediately upon arrival of any aircraft at any place in Botswana and, if not demanded before the time of reporting of such aircraft, the said form shall be submitted to the proper officer at the time of reporting of such aircraft.

(2) The declaration required to be made under section 9 of the Act shall be made individually on the same form by the pilot and every member of the crew of any aircraft.

(3) The pilot and every member of the crew of an aircraft arriving in Botswana directly from a place outside the common customs area may, during the stay of such aircraft, be permitted by the proper officer to retain in his personal possession, and for his personal use, duty free stores in accordance with the following scale—

|

Tobacco |

Potable |

Wine |

Beer |

|

| The pilot |

230 grams |

1 litre |

3 litres |

3 litres |

| Officers |

175 grams |

1 litre |

3 litres |

3 litres |

| Other members |

115 grams |

Nil |

3 litres * |

Nil |

* Only in the case of aircraft belonging to countries where provision is made for wine in the statutory list of provisions or rations.

(4) This regulation shall not entitle the pilot or any member of the crew to land such goods without the payment of duty except with the permission of the proper officer.

(5) If required to do so by the proper officer the pilot or any member of the crew shall produce all sealable goods in his possession.

(6) The proper officer shall place under seal all quantities in excess of those enumerated in subregulation (3), as well as any other goods mentioned in section 9 of the Act or subregulation (7)(and the pilot shall provide every facility for such sealing) but the proper officer may permit the pilot of an aircraft or any member of the crew of an aircraft to leave any sealable stores in his possession on arrival of such aircraft in Botswana in the custody of the proper officer until re-exported under official supervision by such pilot or member of the crew.

(7) The following goods are declared to be sealable goods—

(a) undesirable publications, objects or film;

(b) fire-arms (which include gas and alarm pistols and gas rifles of a calibre of 5,6 mm and larger) and ammunition; and

(c) dangerous weapons (which include swords, daggers, bayonets, knives with cutting edges of 10 cm or more in length (excluding knives for domestic or industrial purposes), loaded or spiked sticks, knuckle-dusters, flick knives, batons of solid rubber, teargas pens and pistols, etc., and walking sticks, etc., which are capable of concealing a blade or any other deadly weapon).

(8) The pilot of an aircraft shall not permit any customs and excise seal on any goods in terms of section 9 of the Act to be broken until the aircraft is en route to a place outside the common customs area without intending to land again at any place in the common customs area.

11. Landing of goods from aircraft; deposit of goods in transit shed

(1) Except as provided in this regulation, goods shall be landed from an aircraft only between the hours of 7.30 a.m. and 5.00 p.m. from Monday to Friday.

(2) The landing of goods shall not be effected at any other time or on Saturdays, Sundays or public holidays, except with the special permission in writing of and under the conditions imposed by the proper officer.

(3) Pilots or their agents requesting permission to land goods from an aircraft at times other than those specified in subregulation (1) or on Saturdays, Sundays or public holidays, shall pay to the proper officer the prescribed charges for the attendance of such officers as the proper officer may deem necessary.

(4) The pilot, agent or the representative of such pilot or agent, or any other person landing goods before due entry thereof, shall remove such goods only into a duly appointed transit shed (or other place previously approved by the Director) and shall stack such goods in such manner as will readily enable a complete check of all packages to be made.

(5) Goods shall not be removed from one transit shed to another without the specific permission of the proper officer.

(6) Goods in transit, or goods marked for another place, shall, on being landed, be kept entirely separate from other goods, and packages which are damaged or from which the whole or part of the contents is missing shall not be placed on board any vehicle for removal to another place until they have been examined in the presence of the proper officer and their contents ascertained.

(7) The packages shall then be repaired to the satisfaction of the proper officer and be sealed by him.

(8) Goods shall, on being landed, not be stacked in the open except with the special permission of the proper officer.

(9) In all cases where landed goods are deposited in the open, the conditions relating to stacking, as stipulated in subregulations (4), (5), (6) and (7), shall apply.

(10) The Director may permit goods which have been duly entered before landing to be landed direct from an aircraft into vehicles for immediate conveyance to their destination on condition that the goods are stowed in the vehicles in such a manner that they can readily be checked.

(11) The Director may permit goods of any class or kind which have not been entered before landing to be landed direct from an aircraft into vehicles on such conditions as he may impose in each case.

(12) If any package landed from an aircraft is leaking or if the whole or part of its contents is missing or if the package is in a damaged condition or the mass of any package differs from the invoiced or manifested mass thereof, the contents of such package (hereinafter referred to as a “discrepant package”), ascertained by examination as stated below, shall subject to section 46(1) of the Act, be accepted as being all the goods imported in such package provided—

(a) such package is examined as early as possible after landing but not later than the expiry of the time referred to in section 40(1) and (2), or removal of such package from the transit shed where it was deposited on landing, whichever is the earlier, or, if not so deposited, before removal from the place where it was landed;

(b) such package is examined, in the case of examination of the package after due entry thereof, by the importer, and in the case of examination of the package before due entry thereof, by the pilot of the aircraft from which it was landed, in the presence of and in conjunction with the proper officer;

(c) an account of the contents of the package (or of the missing goods) issued by the carrier is furnished to the proper officer by the importer or the pilot, as the case may be;

(d) the account is legible and identifies the missing goods to the satisfaction of the Director and is signed and dated by the proper officer, importer or pilot, as the case may be, who conducted the examination;

(e) the account of such discrepant package specifies the identifying marks, numbers and other particulars of each package examined and specifies the actual contents (or the missing goods) of each package separately; and

(f) there is no evidence that the missing goods or any portion thereof entered into consumption in the common customs area, even when the duty on the goods missing therefrom does not exceed P25.

(13) Subregulation (12) shall mutatis mutandis apply in respect of any discrepant package landed from a railway train in which such package was imported and for that purpose any reference to the pilot of the aircraft shall be deemed to be a reference to the carrier of the package.

(14) Subregulation (12) shall mutatis mutandis apply in respect of any discrepant package imported by road and for that purpose any reference in the said subregulation to the proper officer, the pilot of the aircraft, to the time of examination and to any account shall be deemed to be a reference to the proper officer at the place where the conveying vehicle entered Botswana, to the carrier of the package, to the time while such vehicle is under the control of the proper officer at such place and to the account taken by the proper officer of the contents of such package, respectively.

(15) Subregulation (12) shall mutatis mutandis apply in respect of any discrepant package imported by post and for that purpose any reference in the said subregulation to the pilot of the aircraft, to the time of examination and to any account shall be deemed to be a reference to any postal official in whose custody the package is prior to delivery, to the time while such package is in the custody of such official and to an account of the missing goods endorsed by such official on the relative postal manifest respectively:

Provided that the contents of such discrepant package shall be accepted as being all the goods imported in that package even where the duty on the goods missing therefrom does not exceed P25.

(16) Subregulations (12) to (14) shall mutatis mutandis apply in respect of any examination conducted under subregulations (6) and (7), and for that purpose any reference to the pilot of the aircraft and to an account shall be deemed to be a reference to the proper officer and to the account taken by him of the contents of such package, respectively.

(17) Subregulation (12) shall only apply to a discrepant package at the first place of landing thereof in the common customs area and shall not apply to any discrepant package after removal thereof in bond.

(18) Examination, mass-measuring, repairing or removal of any package in terms of this regulation shall, in the discretion of the proper officer, be subject to supervision by him and he may at any time demand re-examination of the package concerned.

12. Delivery of goods from airports and railway goods depots

(1) No person shall deliver goods landed from an aircraft or railway train from any transit shed or other approved place until he has submitted to the authority in control of such shed or other place, a copy of the relative customs and excise delivery order in the form CE.61.

(2) If any goods have been delivered before a valid customs and excise delivery order has been granted by the proper officer in respect of such goods for the delivery or forwarding thereof to the importer, such goods shall, if the proper officer so requires, be returned at the expense of the railway or airline operator to the place from which such goods were so delivered, or be brought to such other place as the proper officer may decide.

(3) The Director may enter into such other arrangements with the railway or airline operators as he may deem necessary in respect of the handling of goods in terms of this Part.

(4) The delivery of goods from any airport or railway transit shed before discharge of the aircraft or train has been completed, will be permitted, provided the customs and excise delivery order proving that the goods have been duly entered has been received by the authority in control of such airport or railway transit shed and the goods are not required to be detained for the purposes of the Department.

(5) No customs and excise delivery order shall be valid and shall be acted upon unless such form is signed and date-stamped by the proper officer and bears the number and date of the bill of entry on which the goods to which such order relates were entered in terms of the Act.

(6) The proper officer may by endorsement on any customs and excise delivery order, or in any other manner, order the detention or the delivery to a place indicated by him of the whole or any part of the goods to which such order relates and such goods shall not be delivered or removed except as ordered by the proper officer.

(7) Every agent, railway official, airline operator or other person landing and delivering goods at any place shall, within a period of 14 days from the date on which such landing commences, or within such further period as the proper officer may allow, furnish to the proper officer a statement with particulars of the packages reported for landing at that place in terms of section 8 of the Act but not landed at the place, and of the packages landed at that place but not so reported, and shall before the expiration of the said period of 14 days or such further period as has been allowed by the proper officer, deliver all goods landed but not reported (unless the said statement reflects particulars of due entry and delivery of such goods), as well as all goods in respect of which due entry has not been made, to the State warehouse or such other place as may be approved by the proper officer.

(1) Any person entering goods for exportation shall, if required to do so by the proper officer, produce all documents relating to the goods together with the air way-bill or consignment note.

(2) Subject to subregulation (6), no person shall cause any goods for export to be loaded into an aircraft, train or any other vehicle unless such person has received a copy of the air way-bill or consignment note relating to such goods, signed and date-stamped by the proper officer, authorising the export of such goods in that aircraft, train or any other vehicle:

Provided that, in respect of air freight cleared at the office of any proper officer, such clearance shall be valid for the export of goods through any customs and excise airport.

(3) Regulation 11(1), (2) and (3) shall mutatis mutandis apply to the exportation of goods by aircraft.

(4) The pilot of any aircraft into which any goods referred to in regulation 8(3) or (4) have been loaded for export shall, before departure from the last place of call in Botswana, on demand by the proper officer indicate to him all such goods for the purpose of checking or account to him for such goods.

(5) No such goods shall be landed at any place in Botswana without the express permission of the proper officer and if landed, such goods shall be treated as imported goods landed without reporting in terms of section 8 of the Act.

(6) In the case of goods being exported from a place in Botswana where there is no customs and excise office, the Director may, in respect of such goods as he considers necessary and under such conditions as he may impose, permit the exporter to present a bill of entry for export of—

(a) goods not ex warehouse in the form CE.23 or 24, together with the relative documents, to the railway or air transport official at that place; and

(b) sales duty goods manufactured in Botswana and exported ex warehouse in the form CE.25 by rail by the licensed manufacturer, together with the relative invoice to the railway official at that place.

(7) Such official shall ensure that the requirements of the Act are complied with before authorising the exportation of the goods in question and shall forward the original of the bill of entry concerned to the Director.

14. Importation or exportation of goods from and to African territories

The importation of any goods from or the exportation of any goods to any African territory with the Government of which any agreement has been concluded under any provision of the Act shall be subject to such agreement.

15. Persons and their baggage entering or leaving the common customs area

(1) A person entering the common customs area shall not remove his baggage, nor any other goods accompanying him, from customs and excise control, or cause such baggage or goods to be so removed until they have been released by the proper officer, and no person shall deliver any such baggage or goods left with or handed to him for delivery until such release has been granted.

(2) Every person entering or leaving the common customs area shall declare unreservedly to the proper officer what goods he has in his possession, taking particular care to mention articles to which attention is invited on the form of declaration approved by the Director.

(3) Every person entering or leaving Botswana shall produce and deliver to the proper officer any goods the importation or exportation of which is prohibited or restricted.

(4) The required declaration shall be made to the proper officer in a form approved by the Director and may be handed to the pilot or any agent clearing the baggage through customs including any representative of the railway operator acting as a clearing agent.

(5) The proper officer may in his discretion accept an oral declaration, but he may subsequently demand a written declaration.

(6) Any goods brought into the common customs area and intended for sale shall be specially declared as cargo and shall be entered as such for customs and excise purposes on the specified forms.

(7) Any goods not being cargo reported in terms of section 8 of the Act which have been imported or exported or removed from customs and excise control or in respect of which an attempt at importing, exporting or removal has been made without a valid declaration shall be treated as goods imported, exported or removed without due entry thereof.

16. Rent to be paid on goods in a State warehouse

The charge for rent on goods (except state stores) in any state warehouse in Botswana shall, depending upon the circumstances, be calculated as follows—

(a) goods landed at a place to which they were not consigned, at the rate of 50 thebe per 100 kg or portion thereof for every seven days or portion of seven days;

(b) goods imported by an individual and which are seized in terms of the provisions of section 99(1) of the Act and subsequently delivered in terms of section 104 of the Act, at the rate of 20 thebe per 10 kg or portion thereof for every seven days or portion of seven days;

(c) goods imported by an individual and which are seized in terms of the provisions of section 124(1) of the Act pending the production of a certificate, permit or other authority and subsequently released in terms of section 118 of the Act, at the rate of 20 thebe per 10 kg or portion thereof for every seven days or portion of seven days;

(d) goods which are removed within 14 days from the date of receipt, at the rate of P1,00 per 100 kg or portion thereof for every seven days or portion of seven days;

(e) goods which are removed after 14 days but within 28 days from the date of receipt, at the rate of P2,00 per 100 kg or portion thereof for every seven days or portion of seven days;

(f) goods which are removed after 28 days from the date of receipt, at the rate of P4,00 per 100 kg or portion thereof for every seven days or portion of seven days; or

(g) unentered goods which are sold in terms of the provisions of section 45(4) of the Act, at the rate of P2,00 per 100 kg or portion thereof for every seven days or portion of seven days:

Provided that the Director may in any special circumstances, rebate the rental charge to such extent as he may in his discretion decide.

(1) All goods removed in bond under section 17(1) of the Act shall be entered for removal on a bill of entry for removal in bond in the form CE.14 or 15, but the Director may, in respect of such class or kind of goods as he may decide, accept such other form of entry as he may approve on such conditions as he may impose.

(2) Subject to subregulations (9), (10) and (11), no goods shall be removed in bond until the remover has been authorised by the proper officer on a landing, delivery and forwarding order or other document to remove such goods.

(3) Goods may be removed in bond within the common customs area only to a place appointed as a place of entry or, in circumstances which the Director considers to be exceptional, to any railway station or siding, or any premises or warehouse within the area of control of the proper officer at that place or, in the case of excisable goods, to a licensed customs and excise warehouse if such goods are intended for warehousing in such customs and excise warehouse:

Provided that sales duty goods manufactured in Botswana may be removed in bond only to a place appointed as a place of entry and only for re-warehousing at that place.

(4) Except where otherwise provided in these Regulations, the consignee of goods removed in bond to a place in the common customs area shall not take delivery of such goods or cause them to be warehoused or exported at the place of destination until he has duly entered the goods at the customs and excise office at that place, for consumption, warehousing or export, and has obtained the written authority of the proper officer for such delivery, warehousing or export.

(5) The said consignee shall also submit to the proper officer all such invoices and documents relating to the goods as he may require as well as a numbered and date-stamped copy of the relative bill of entry for removal in bond.

(6) If entry of the goods at the place of destination is not made within seven days of the arrival of the goods at that place, or within such further period as the proper officer may allow, the remover or the carrier or other person having custody of the goods shall forthwith deliver them to the State warehouse or other place approved by the proper officer.

(7) Any person removing goods in bond to a place in the common customs area shall consign the goods to the care of the officer in charge of customs and excise at that place and shall conspicuously mark the consignment note with the words “In Bond”.

(8) The carrier shall advise its officials or agents at the place of destination that the goods are in bond and shall not deliver the goods without the written authority of the proper officer.

(9) Subject to subregulation (11), the Director may, in the case of goods in transit through Botswana from any other territory in Africa by air or rail to any destination outside the common customs area, allow the goods in question to be entered for removal, in the case of goods removed by air, at the place where the goods are first landed in the common customs area, or in the case of goods removed by rail, at the place where the goods are exported from the common customs area provided the duty on any deficiency is paid forthwith.

(10) No person shall allow such goods to be carried forward or exported from such airport or place until such goods have been duly entered for removal in bond and the proper officer at the place in question has granted written authority for such carriage or export.

(11) Goods in transit overland through Botswana from any other territory in Africa other than by air or rail shall be catered for removal in bond at the place where they enter Botswana.

(12) Except with the permission of the Director, goods in transit through the common customs area to a destination outside the common customs area shall be exported immediately and if export cannot take place immediately such goods shall be warehoused in a licensed customs and excise warehouse after entry for warehousing.

(13) Beef or other meat and such other goods as the Director may decide, in transit by rail through the common customs area to a destination outside the common customs area shall be carried in sealed trucks direct from the sending station to the place of export in Botswana and such seals shall not be broken except with the permission of the proper officer at that place.

(14) Such goods carried by any other means shall be subject to such conditions as the Director may impose.

(15) Goods removed in bond to a customs and excise warehouse for manufacturing purposes or for storage in such warehouse shall be entered on a bill of entry for warehousing or re-warehousing but goods removed in bond to a place of entry for any other purpose may be duly entered for such purpose even if removed to such place from a customs, excise and sales duty warehouse in terms of section 20(7)(c) of the Act.

(16) The following particulars shall be reflected on a bill of entry for direct removal in bond in the form CE.14—

(a) in the case of goods removed in bond to a place outside the common customs area, full particulars as required in accordance with the bill of entry form;

(b) in the case of goods which have been landed from an aircraft or other vehicle at a place to which they were not consigned and are removed in bond by the pilot or other carrier to the place to which they were consigned in the first place, full particulars as required in accordance with manifest requirements in the forms CE.2 and 3 and such additional particulars as are available to such pilot or other carrier in respect of such goods; and

(c) in other cases, full particulars as required in accordance with the bill of entry form, but the particulars relating to tariff heading or item or both need not be furnished unless required to be furnished by the Director.

(17) Suppliers’ invoices in respect of goods entered for removal in bond in the circumstances stated in subregulation (16)(a) shall be produced to the proper officer at the time of entry for removal, and suppliers’ invoices, documents of title and such other documents as may be required by the proper officer shall be produced to the proper officer at the time of due entry at the place of destination in respect of goods removed in the circumstances referred to in subregulation (16)(b) or (c).

(18) If goods which have been entered for warehousing at the place of importation are required for immediate removal in bond from that place before they have been deposited in the warehouse, they may be treated and entered for removal as if they had been so deposited.

(19) If the final destination of any goods is a place other than the place of entry to which such goods have been removed in bond, no person shall remove such goods or cause such goods to be removed from such place of entry until such goods have been duly entered and, the proper officer has granted written authority for delivery thereof and if forwarded to the final destination without such written authority, such goods shall, if the proper officer so requires, be returned at the expense of the carrier or other person who brought the goods into the common customs area or who removed the goods without such written authority, to such place of entry or to such other place as the proper officer may decide.

PART IV

Customs and Excise Warehouses: Storage and Manufacture of Goods

in Customs and Excise Warehouses (regs 18-38)

18. Approval of customs and excise warehouses

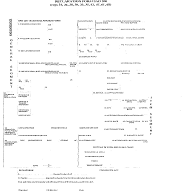

(1) Customs and excise warehouses (excluding special customs and excise manufacturing warehouses) shall be licensed only at places appointed in terms of section 7 of the Act and on application on forms CE.100 and 100A.

(2) Forms CE.100 and 100A shall be completed in all details and shall be accompanied by such plans, description of the warehouse or other particulars as the Director may require.

(3) A licence for a customs and excise warehouse may be issued in respect of any premises, store, fixed vessel, fixed tank, yard or other place which complies with such conditions as the Director may impose in each case in regard to construction, situation, access, security or any other condition he considers necessary.

(4) Different premises, stores, vessels, tanks, yards, or other places on a single site, or on more than one site approved by the Director, may be licensed as a single customs and excise storage warehouse, a single customs and excise manufacturing warehouse, or a single special customs and excise warehouse for the purpose of sales duty in the name of one licensee.

(5) Separate customs and excise warehouses on the same site may be licensed in the names of different persons subject to the conditions referred to in subregulation (3).

(6) The Director may license a customs and excise warehouse for the storage or manufacture of any particular commodity or article or any class or kind of commodity or article and such warehouse shall not be used for any other purpose, except with the written permission of the Director.

(7) If the security for the duty is at any time in the opinion of the proper officer not sufficient in regard to any customs and excise warehouse in which goods are deposited, he may at the risk and expense of the licensee of such warehouse and the owner of such goods cause them to be immediately removed and deposited in another customs and excise warehouse or other place approved by him; alternatively, the said licensee or owner may forthwith pay the duty on the goods.

(8) The licensee of a customs and excise warehouse shall keep at the warehouse, in a place accessible to the proper officer, a record in a form approved by the Director of all receipts into and deliveries or removal from the warehouse of goods not exempted from entry under section 20(6) of the Act, with such particulars as will make it possible for all such receipts and deliveries or removals to be readily identified with the goods warehoused, and with clear references to the relative bill of entry passed in connection therewith.

(9) The licensee of a customs and excise warehouse shall display in a prominent position in the warehouse an extract of the relative regulations in this Part.

(10) No goods entered for storage or manufactured in a customs and excise warehouse (except spirits or wine in the process of maturation or maceration in a customs and excise manufacturing warehouse) shall be retained in customs and excise warehouses for a total period of more than five years from when the goods were first entered for warehousing but the Director may, in exceptional circumstances and on such conditions as he may impose in each case, allow such goods intended for trade purposes to be so retained for a further period not exceeding one year and such other goods as he may decide to be retained for such further period as he may specify.

(11) Any fixed vessel, tank, receiver, vat or other container licensed as a customs and excise warehouse or used in a customs and excise warehouse for the storage or manufacture of any goods in terms of Part IV of the Act shall be gauged in a manner approved by the Director and any fitting, meter, gauge or indicator necessary for ascertaining the quantity of any goods contained in such vessel, tank, receiver, vat or other container shall be supplied and fitted by the licensee at his expense.

(12) The licensee of a customs and excise warehouse shall notify the proper officer immediately of, or prior to, any change, or contemplated change, no matter of what nature, in his legal identity, name or address of his business or goods manufactured by him.

19. Storage of goods in customs and excise warehouses

(1) Subject to subregulations (3) and (4), goods which have been entered for warehousing in a customs and excise warehouse shall be conveyed to the warehouse immediately after such entry and there deposited.

(2) All goods entered for warehousing shall be conveyed to the warehouse only by the railway operators or by a person who has given such security as the Director may require in terms of section 111 of the Act.

(3) Imported packages which have been entered for warehousing in a customs and excise warehouse but which are leaking, or of which the whole or part of the contents is missing, or which are in an otherwise damaged condition, shall not be removed to the warehouse unless examined in terms of regulation 11(12) to (17).

(4) If such package is however removed to the warehouse without such examination the full invoiced contents of such package shall be deemed to have been imported and shall be accounted for under the provisions of the Act.

(5) The licensee of any customs and excise warehouse shall notify the owner of any imported goods entered for warehousing in such warehouse of the non-receipt of any such goods, or any part thereof, and the owner of such goods shall take immediate steps to account to the proper officer for such goods or to pay the duty due thereon.

(6) The licensee of any customs and excise warehouse into which goods are received shall ensure that such goods have been duly entered for warehousing in such warehouse and, unless proof that such goods have been so entered is in his possession at the time of receipt of such goods, he shall keep such goods separated from other goods in such warehouse and make a report to the proper officer forthwith.

(7) The licensee of a customs and excise warehouse shall not allow any goods of a dangerous or inconvenient nature to be stored in such warehouse unless it has been approved for the storage of such goods, and the licensee of a customs and excise warehouse which has been approved for a particular class of goods shall not allow any other goods to be deposited therein.

(8) All goods in a customs and excise warehouse shall be so arranged and marked that it will be easily identifiable and accessible for inspection and that each consignment and the particulars thereof can readily be ascertained and checked.

(9) Goods deposited in a customs and excise warehouse may at any time be examined by the proper officer and the licensee of such warehouse, or his representative, shall be present during such examination and assist the proper officer in the execution of such examination.

(10) Goods deposited in a customs and excise warehouse in closed trade containers shall not be examined, nor the packages opened or altered in any way, except with the permission of the proper officer and in the presence of an officer if he so requires, unless immediate action for the safety of the goods is necessary, in which case the licensee shall immediately notify the nearest available officer.

(11) No unpacked goods in liquid form shall be stored in ungauged containers in a customs and excise warehouse without the written permission of the Director.

(12) Subject to section 22 of the Act, samples of warehoused goods, in such quantities as the proper officer may allow, may be taken by the importer under customs supervision, provided that prior written application is made.

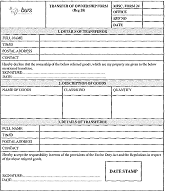

20. Transfer of ownership of dutiable goods in warehouse

The transfer of ownership of dutiable goods in a customs and excise warehouse shall only be acknowledged if the prescribed form is presented to the proper officer duly completed in all respects and is supported by or includes a declaration as indicated hereunder—

(a) “I, ……………………………………. for transferor, hereby declare that ownership of the above-mentioned goods, which are my property, is given to …………………………………………… address ……………………………………….;

For transferor ………………………………………………………. Date ………………..”.

(b) “I ……………………………………. for transferee, hereby accept responsibility in terms of the provisions of the Customs and Excise Duty Act, and regulations in respect of the above-mentioned goods.

For transferee ………………………………………………………. Date ……………….”

21. Manufacture of goods in customs and excise warehouses

(1) The Director may, on such conditions as he may impose in each case, allow the manufacture by a licensee in a customs and excise manufacturing warehouse of goods which shall not be subject to the provisions of Part IV of the Act.

(2) Subject to regulation 18(2), any application for the licensing of a customs and excise manufacturing warehouse shall state the nature of materials and the processes to be used in the manufacture of every excisable or other product, the expected annual quantities of such materials to be so used and the expected annual production of every excisable product:

Provided that the nature and quantity of materials to be used in the manufacture of sales duty goods need not be stated.

(3) The plans referred to in section 27(5) of the Act shall be submitted to the Director with as many copies as he may require.

(4) Distinguishing marks or numbers to the satisfaction of the Director shall be indicated on every room, vessel, still, utensil or other plant and such mark or number shall be shown on schedules submitted with such plans.

(5) Vessels, stills and other plant in a customs and excise manufacturing warehouse shall be placed, fixed and connected to the satisfaction of the Director and the licensee shall not alter the shape, position or capacity of any plant or install any additional or new plant or remove any plant without the permission of the Director after submission to him of an application for alteration of such plant.

(6) No manufacturing shall commence in a customs and excise manufacturing warehouse without the permission of the Director.

(7) All rooms, places, distilling apparatus, spirits receivers and other fixed vessels or containers and such other plant as the Director may specify, in a customs and excise manufacturing warehouse shall be locked or otherwise secured in accordance with the instructions and in the discretion of the proper officer, and the licensee shall at his own expense and to the satisfaction of the proper officer, provide, apply, repair and renew whatever is required to enable the proper officer to affix locks to such rooms, places, distilling apparatus, spirits receivers and other fixed vessels or containers and other plant specified by the Director, or to secure them in any other manner.

(8) Every pipe in a customs and excise manufacturing warehouse shall, except with the permission of the Director or unless used exclusively for the discharge of water and spent wash, be so fixed and placed as to be capable of being examined for the whole of its length.

(9) Pipes for the conveyance of different materials or products shall, if required by the Director, be painted in such colour for every material or product as he may require.

(10) The licensee shall paint such pipes at his own expense and shall repaint such pipes whenever required by the proper officer.

(11) Every cock and valve used in such warehouse shall be of a type approved by the Director.

(12) The licensee shall keep such cocks and valves in proper repair at all times.

(13) No person other than a licensee of a customs and excise manufacturing warehouse licensed for the manufacture of excisable goods shall own, use or control a machine for cutting tobacco or a machine, appliance or apparatus which is in the opinion of the Director of a type specially designed for any process in the manufacture of an excisable product except with the permission of the Director and no person to whom permission to own, use or control such machine, appliance or apparatus has been so granted, shall sell or dispose of such machine, appliance or apparatus or allow any other person to use it without the permission of the Director.

(14) The Director may require that any class or kind of such machine, appliance or apparatus shall be registered with him and shall bear such registration numbers in such manner as he may decide.

(15) When a manufacturing operation has been completed in a customs and excise manufacturing warehouse, the licensee shall give the proper officer all the necessary assistance in ascertaining the quantity and strength or other particulars of the goods manufactured and record such particulars and render such returns as the Director may require.

(16) A licensee shall stop any operation or the working of any still when required to do so by the proper officer for the purpose of testing the output.

(17) Every licensee who is required to do so by the Director shall furnish a diagram to scale of any still, utensil or other plant in his customs and excise manufacturing warehouse together with explanatory notes relating to the working of such still, utensil or other plant.

(18) Except with the permission of the proper officer, no excisable goods manufactured in a customs and excise manufacturing warehouse shall be removed from a receiver, vessel or other container in which they were collected until account thereof has been taken by the proper officer.

(19) The Director may allow the quantity of any excisable goods in a customs and excise manufacturing warehouse to be ascertained by means of any massmeter, meter, gauge or other instrument or appliance of a type approved by him.

(20) The licensee shall supply and fit such massmeter, meter, gauge or other instrument or appliance to the satisfaction of the Director and keep it in proper repair at his expense and shall have it assized regularly and, in addition, at any time required by the proper officer.

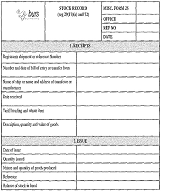

(21) Every licensee of a customs and excise manufacturing warehouse shall, unless exempted by the Director, keep a stock record, in a form approved by the Director, in which such licensee shall record daily such particulars of receipts of materials, nature and quantities of excisable goods manufactured, nature and quantities of by-products or other goods manufactured and disposal of goods manufactured and such other particulars as the Director may require in each case.

(22) Such stock record shall, when not in use, be kept in a fire-proof safe.

(23) Every licensee of a customs and excise manufacturing warehouse shall furnish to the proper officer such returns showing such particulars and at such times and under such conditions as the Director may decide.

(24) Subregulations (3) to (12) and (15), (16) and 21 and (22) shall not apply in respect of special customs and excise warehouses for purposes of sales duty.

22. Clearance and removal of goods from customs and excise warehouses and payment of duty

(1) The licensee of a customs and excise warehouse shall not cause or permit any goods to be delivered or removed from such warehouse until he is in possession of a relative ex-warehouse bill of entry, in the specified form, numbered and date-stamped by the proper officer, and any person entering any goods for delivery or removal from a customs and excise warehouse shall do so on the forms specified herein.

(2) Notwithstanding subregulation (1) and subject to the Sixth Schedule hereto the Director may permit the licensee of any customs and excise warehouse to remove from such warehouse goods which are liable to excise duty or sales duty or both, or such other goods as the Director may specify from time to time, provided—

(a) a certificate for removal of excisable or specified goods ex-warehouse in the form CE.32, duly completed by the licensee of such warehouse, is deposited by such licensee in the entry box referred to in subregulation (3);

(b) in the case of sales duty goods manufactured in Botswana, an invoice prescribed in subregulation (19) and regulation 33(12) and (13) is completed or complies with regulation 13(6); and

(c) he complies with subregulations (5), (6), (7), (8), (9), (10), (12), (13) and (16).

(3) Except with the permission of the Director, subject to such conditions as he may impose, every licensee of a customs and excise warehouse who has been granted permission in terms of subregulation (2) shall provide and fix to any convenient and permanent structure in an accessible place in such warehouse an entry box of a construction and design approved by the Director, for safe depositing of documents.

(4) The box in question shall be provided with fittings and shall be designed to enable the proper officer to lock it with a State lock so that documents deposited therein cannot be withdrawn and also so that at any time considered necessary by the Director documents can neither be deposited nor withdrawn.

(5) In the case of excisable goods to be removed from any customs and excise warehouse for home consumption under Schedule No. 6 of the Act or for the home consumption as State stores, the licensee of such warehouse shall, notwithstanding subregulation (2), not remove or permit such goods to be removed from such warehouse unless a declaration regarding restricted removal of excisable or specified goods ex-warehouse in the form CE.33 has been completed and signed by the manufacturer under Schedule No. 6 of the Act or an official of the state body in question, as the case may be, and a copy of such declaration has been attached to each copy of the certificate for removal of excisable or specified goods ex-warehouse in the form CE.32.

(6) In the case of goods to be so removed for consumption under Schedule No. 6 of the Act, the Director may require that the said declaration shall be approved by the proper officer in the area where the manufacturer’s premises are situated before such goods are removed.

(7) Joint excise and sales duty accounts together with the bills of entry as referred to in subregulation (1) shall be presented to the proper officer by the licensee of each customs and excise warehouse in respect of all motor vehicles which are subject to excise and sales duty and removed from such warehouse during the previous period of three months for the purposes mentioned in section 20(7) of the Act on or before the 14th day of the month following the period of three months to which the account relates.

(8) All other bills of entry as referred to in subregulation (1) shall be presented to the proper officer by the licensee of each customs and excise warehouse in respect of all excisable or specified goods removed from such warehouse during the previous calendar month for the purposes mentioned in section 20(7) of the Act within 14 days after stock-taking or the closing of accounts for duty purposes.

(9) Copies of all certificates (including certificates and invoices in respect of motor vehicles) deposited in the entry box for each such purpose or for each class or kind of bill of entry specified in these Regulations, as the Director may require, shall be attached to the original of the respective bills of entry or shall be specified on a schedule attached to such bill of entry, such certificates being submitted to the proper officer separately in accordance with conditions which the Director may impose.

(10) Any duty due in respect of goods to which such bills of entry relate shall be paid by such licensee.

(11) Notwithstanding subregulation (1) the Director may also permit the licensee of a customs and excise warehouse, subject to compliance with the requirements of subregulations (3) and (4), to remove from such warehouse imported oil classified under tariff headings 27.07.50, 60, 70 of 80 and 27.10.20, .30, .40 or .50 and such other imported goods as the Director may permit from time to time, for consumption in terms of item 401.00 under subregulations (2) to (10) and in that event the said subregulations (2) to (10) shall mutatis mutandis apply and for the purpose of such application any reference in such regulations to excisable goods and excise duty shall be deemed to be a reference to the above-mentioned goods and to fiscal and customs duties or fiscal and customs duties as well as excise duty, respectively.

(12) Certificates may be deposited in the entry box in his customs and excise warehouse by a licensee at any time during the hours when goods are permitted to be delivered or removed from such warehouse, but the Director may require in writing that certificates relating to deliveries or removals from such warehouse for any date or any period stated by the Director shall be deposited in the entry box before a time indicated by him on that date or on each day during that period.

(13) The licensee shall number certificates consecutively in the space provided in respect of removals from each customs and excise warehouse.

(14) When the proper officer has authorised the delivery or removal of any goods from a customs and excise warehouse or the licensee has deposited a certificate in terms of subregulation (2) in the entry box for delivery or removal of any such goods, the licensee of the warehouse shall cause such goods to be so delivered or removed immediately, unless the special permission of the proper officer has been obtained for their retention, but for any retention exceeding a period of seven days the permission of the Director shall be obtained.

(15) The Director may grant general permission for retention in respect of such class or kind of goods and for such periods as he considers necessary.

(16) The duty on any goods removed from a customs and excise warehouse shall be payable before such goods are so removed, but in respect of goods removed under subregulation (2) the Director may, subject to such security as he may require and to such conditions as he may impose in each case, permit the payment to be deferred to such date or dates as the Director may determine.

(17) Notwithstanding the provisions of subregulation (16), every manufacturer of sales duty goods or excisable goods of Section B of Part 2 of Schedule No. 1, every owner of sales duty goods or such excisable goods manufactured for him partly or wholly from materials owned by such owner, and every manufacturer of and dealer in pearls, precious and semi-precious stones, precious metals or articles containing or manufactured of such pearls, precious and semi-precious stones or precious metals, shall present quarterly an account, in accordance with the directions of the Director, in respect of any goods removed from their premises which have been licensed as special customs and excise warehouses for the purposes of sales duty or such excise duty.

(18) The said account shall be presented to the proper officer and the duty due paid to him on or before the 25th day of the month following the quarter to which the account relates:

Provided that, in the case of motor vehicles, accounts shall be presented and the duty paid at the times prescribed in subregulations (7) to 10 and (16) respectively.

(19) Regulation 33(12) and (13) shall mutatis mutandis apply in respect of any removal of sales duty goods ex-warehouse and for that purpose any reference to beer shall be deemed to be a reference to any sales duty goods.

(20) On any duty paid after the dates mentioned in subregulations (16), (17) and (18) interest shall be paid at the rate of 10 per cent per annum for every full month the amount is in arrear, a portion of a month being calculated as a full month:

Provided that the Director may, in his discretion, remit such interest if he is of the opinion that circumstances exist on account of which such arrear payment was unavoidable.

23. Clearance and removal of goods from customs and excise warehouses for home consumption

(1) Excisable goods shall not be removed from any customs and excise warehouse for payment of duty in terms of regulation 22(1) or (2) except in such minimum quantities as the Director may determine in respect of each excisable product or spirituous beverage.

(2) Subject to regulation 22(11) imported goods liable to fiscal and customs duty or sales duty or both shall not be removed from a customs and excise warehouse for home consumption until such goods have been entered in terms of section 20(7) of the Act with payment of any duty due and the licensee of such warehouse is in possession of a copy of such entry numbered and date-stamped by the proper officer.

24. Clearance and removal of goods from customs and excise warehouses for export (including supply as stores to foreign-going aircraft)

(1) The clearance and removal of goods from any customs and excise warehouse for export or supply as stores to any foreign-going aircraft shall be subject to regulation 22(1) to (16).

(2) The proper officer may require any goods entered for export or supply as stores from any customs and excise warehouse to be delivered to any examination shed or other place indicated by him or may require such goods to be retained in such warehouse for the purpose of examination prior to such export or supply and such goods shall not be removed, exported or supplied without the permission of the proper officer.

(3) The goods in question shall be kept separate from any other goods conveyed on the same vehicle and shall be accompanied by a copy of the relative bill of entry, certificate or invoice mentioned in regulation 22(2).

(4) Unless the stores are conveyed by the actual remover or owner or licensee of the customs and excise warehouse in question or his employee, such stores shall, except with the permission of the Director, be carried only by the railway operators or a person who has given security in terms of section 111 of the Act.

(5) Such goods for export or supply as stores shall be presented to the proper officer, at such place as the officer may decide for verification and immediately thereafter be conveyed by the shortest route to the aircraft or rail by means of which they will be exported.

(6) No carrier or other person shall divert such goods to any other destination or substitute any other goods for such goods intended for export or supply as stores or tamper with such goods in any manner.

(7) The licensee of a customs and excise warehouse from which goods for supply to a foreign-going aircraft as stores are removed, shall obtain on a copy of the bill of entry, certificate or invoice relating to such goods a receipt signed by an officer of the aircraft to the effect that the stores have been received on board, and such receipted copy shall be handed to the proper officer before the departure of the aircraft.

(8) The licensee shall produce proof to the satisfaction of the Director that goods entered for export or supply as stores to a foreign-going aircraft have been exported and such proof shall be submitted within such period as the Director may require.

(9) If any goods removed from a customs and excise warehouse for export or supply as aircraft stores, or any portion of such goods, are not shipped or despatched, the licensee of the said warehouse shall immediately report the facts to the proper officer and he shall forthwith pay the duty on such goods or cause them to be removed to the State warehouse or take such other action as the proper officer may decide.

(10) The pilot of an aircraft shall produce any stores on board his aircraft (irrespective of where such stores were taken on board) whenever and wherever he is required to do so by the proper officer, and shall provide facilities for such stores to be placed under seal.

(11) He shall also forthwith pay the duty on any stores which were shipped outside the common customs area or which were shipped at any place in the common customs area ex customs, excise and sales duty warehouse and which have been consumed, sold or disposed of on such aircraft at any place in the common customs area when the aircraft is not air-borne or on such aircraft on a flight between any places in the common customs area (except such stores which have been so consumed for the operation of the aircraft itself or which have been so consumed by the pilot or any member of the crew or any passenger as part of the service included in the service contract of such pilot or crew member or fare of such passenger without extra payment therefor).

(12) For the purposes of subregulation (1) goods which may be supplied to an aircraft as stores shall include all consumable goods normally used on such aircraft for propulsion, catering or maintenance but shall not include normal durable equipment or replacements of normal durable equipment of such aircraft.

(13) Normal durable equipment or replacements thereof shipped at any place in the common customs area on any foreign-going aircraft shall, except if elsewhere provided for, be treated as an export of such goods and shall be subject to the provisions of the Act and these Regulations insofar as they relate to the exportation of goods.

25. Clearance of goods from customs and excise warehouses for removal in bond

(1) Regulation 17 shall mutatis mutandis apply to goods removed in bond from any customs and excise warehouse.

(2) The removal in bond of goods from a customs and excise warehouse shall also be subject to regulation 22(1) to (16).

(3) In the case of goods liable to excise duty only and removed in bond from one customs and excise warehouse to another, any copy of a certificate for the removal of excisable or specified goods ex-warehouse in the form CE.32 relating to the removal of such goods shall, on being deposited in the entry box in such warehouse to which such goods were so removed, be deemed to be a bill of entry for re-warehousing in respect of such goods in that warehouse.

(4) In the case of sales duty goods manufactured in Botswana, the owner may only remove such goods in the form CE.32 for removal in bond and for re-warehousing only.

(5) Particulars of such removals shall be indicated on a form as required by the proper officer.

(6) The consignee of any goods removed in bond shall notify the remover immediately of the non-receipt of such goods, or any part thereof, and such remover shall take immediate steps to account to the proper officer for such missing goods or to pay the duty due thereon.

26. Ascertaining the strength and quantity of spirits for duty purposes

(1) The strength of any spirits or any spirituous preparation imported into or manufactured in Botswana shall be ascertained in the manner specified by the Director.

(2) In any entry, certificate, return, invoice, statement or other document submitted to the department in accordance with the provisions of the Act in respect of imported spirits or spirituous preparations, or spirits or spirituous preparations manufactured in Botswana, the strength of such spirits or spirituous preparations shall be declared as percentage alcohol by volume at 20° Celsius.

(3) The quantity of spirits in any container shall, if calculated by mass-measuring, be ascertained in the manner specified by the Director.

27. Control of the use of spirits for certain purpose

(1) Samples for reference to the Director in terms of section 30(1) of the Act shall, whenever possible, be taken by, or under the supervision of the proper officer, and shall be despatched in a manner determined by the Director.

(2) The licensee concerned shall furnish such declaration and in such form as the Director may require.

(3) The Director shall set forth in a certificate his decision concerning the certification or approval of any sample submitted.

(4) No person shall, without authority of the proper officer, tamper with, substitute or alter any sample or a label thereon after such sample has been taken for certification or approval.

(5) A licensee who intends using for blending brandy in terms of section 30(2) of the Act any spirits in respect of which a rebate of duty for maturation is provided for, shall notify the proper officer at least 24 hours before commencement of such blending operation and comply with such conditions regarding supervision of the blending operation as he deems necessary.

(6) Where the proper officer directs that an officer should be present at the blending operation, the blending must take place under the supervision of the officer.

28. Requirements in respect of stills

(1) Subject to subregulation (2) no person, other than an agricultural distiller, shall use a pot still with a capacity of less than 680 litres or a continuous still which is not capable of distilling 910 litres or more of wine or wash per hour.

(2) Subregulation (1) shall not apply to any still lawfully in use at the time of the commencement of the Act, or to any still which the Director may, in his discretion, authorise to be used for the distilling or manufacture of essences or such other preparations as he may determine, or for experimental purposes.

(3) No agricultural distiller shall use a still with a capacity of less than 90 litres for distilling spirits:

Provided that this requirement shall not apply in respect of a still which is lawfully in the possession of an agricultural distiller immediately prior to the commencement of the Act.

(4) No person shall use a still for distilling spirits, and no licence to distil spirits therein shall be issued, unless such still is made wholly of copper, tin, stainless steel or aluminium.

(5) The said stills shall only be repaired with one or more of the aforementioned metals (not coatings thereof) unless otherwise approved by the Director.

(6) When an agricultural distiller ceases to operate as an agricultural distiller or ceases to be an agricultural distiller in terms of the Act, he shall, in addition to any notification under any provision of the regulations regarding any spirits manufactured by him, forthwith notify the Director of the disposal or intended disposal of any still in his possession.

29. Spirits manufactured by agricultural distillers

(1) An agricultural distiller shall not use a still which is not erected on a foundation of brick, stone or cement and is not securely built-in to the satisfaction of the proper officer and in a position approved by him on the farm in question.

(2) Every agricultural distiller shall submit on forms approved by the Director—

(a) to the proper officer within 30 days after the first day of January in each year, a return of spirits in his possession on the first day of January;

(b) to the proper officer within 14 days after completion of each new distillation or re-distillation of spirits by him, a return of the quantity and strength of the spirits so distilled or re-distilled; and

(c) on demand by the proper officer, a return, declared by him to be correct, of the strength and quantity of spirits in his possession on the date of such demand.

(3) The return required in terms of subregulation (2)(a) shall also be rendered by a person who has ceased to be an agricultural distiller, but who was an agricultural distiller the preceding calendar year.

(4) When an agricultural distiller ceases to operate as an agricultural distiller or ceases to be an agricultural distiller in terms of the Act, he shall notify the Director forthwith and furnish at the same time a return of the nature referred to in subregulation (2)(c) on the date on which he ceases to operate as or to be an agricultural distiller.

(5) He shall also pay the duty forthwith on any spirits stated in such return to be in his possession on such date, unless such spirits are consumed on such farm in accordance with the Act, and shall surrender to the proper officer the counterfoils of any certificates issued in respect of any spirits, as well as any unused certificates in his possession.

(6) Regulations 21(1) to (22), 22(1) to (16) and 30(1) to (5) shall mutatis mutandis apply to any agricultural distiller and to any spirits manufactured by him, and for the purpose of such application any reference to a customs and excise manufacturing warehouse shall be deemed to be a reference to the farm owned or occupied by such agricultural distillers or on which such spirits are manufactured, but the Director may exempt any class of agricultural distillers from the application of all such regulations or any such regulation on such conditions as he may impose in each case.

30. Manufacture of spirits in customs and excise manufacturing warehouses